This article examines the Cement Sector in Pakistan and explores the publicly listed companies currently listed on the Pakistan Stock Exchange. It discusses the revenue growth, market capitalisation, and net profitability trends over the last 5 years.

Cement is literally the mortar that founds and establishes any industrial capacity or national progress. It would be impossible to create and maintain dams, highways, housing schemes and otherwise increase industrial ability in any nation.

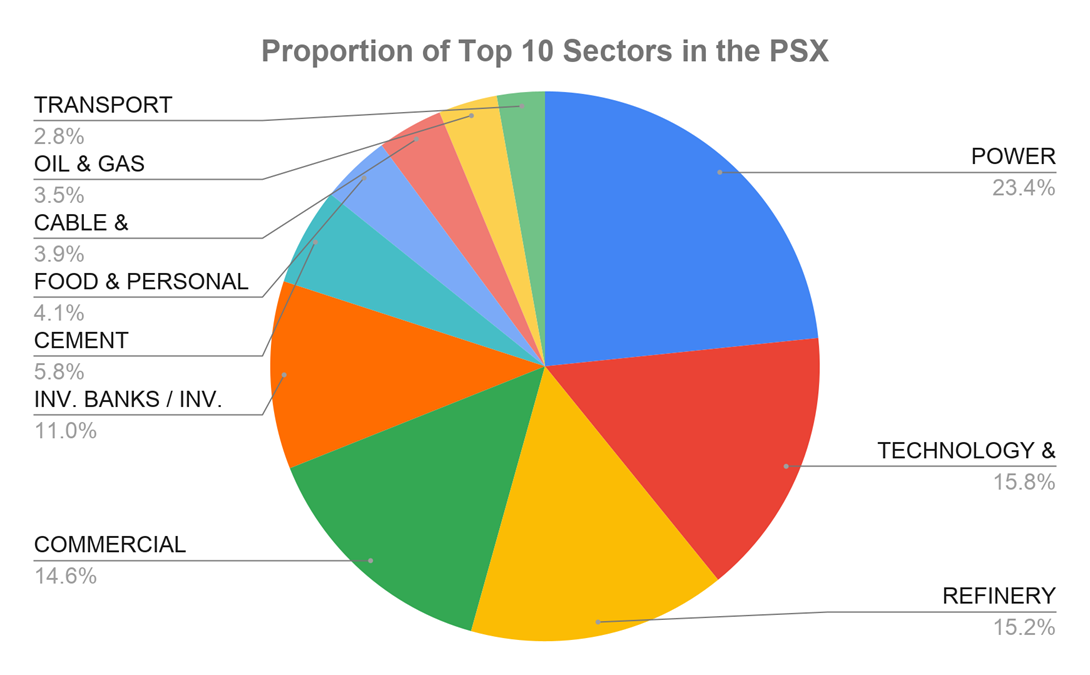

In Pakistan, Cement and its assorted materials, such as clinkers and concrete mixes, are produced by both publicly listed companies and private family enterprises. Cement Sector is listed in the Pakistan Stock Exchange and currently 21 companies are licensed under the sector code. It is the 7th Largest Sector in terms of Market Capitalization in the Pakistan Stock Exchange. Here is a greater view of where it fits.

Sector’s Revenue & Profitability 2025

The cement sector has been growing as one of the most prominent sectors in Pakistan with majority of the growth of the publicly listed companies coming from exports, and as they switch their focus to that private enterprise have stepped in to meet the local demand.

This movement to be paid in foreign currency is the reason why the cement sectors revenue has increased, alongside its median Net Profit Margins across the industry. This is in stark contrast to traditional growth where in the growth phase of the industry, the margins suffer.

Below is the table of a comparison of the revenue growth over the last 5 years, in Pakistan Rupees.

| Year | Total Revenue | Growth |

| 2021 | Rs. 361.6 billion | |

| 2022 | Rs. 498.7 billion | 27.49% |

| 2023 | Rs. 603.9 billion | 17.42% |

| 2024 | Rs. 671.1 billion | 10.02% |

| 2025 | Rs. 712.4 billion | 5.80% |

The Chart (Revenue 1) of the sector shows that in the last 5 years that the combined revenue of all the companies currently listed in the stock exchange’s cement sector has not only risen at a dependable rate but also nearly doubled since 2021. However, if we take a closer look, at the individual revenues generated by these companies (Revenue 2). We will clearly see that the majority of these revenues are by single big players such Bestway Cement, Lucky Cement and Fauji Cement, D.G.Khan Cement and Maple Leaf Cement. All of these are contributing to a total of Rs. 712.4 billion in Sector revenue, most of which is internationally exported and received in foreign currency. This is what is providing us with the growth

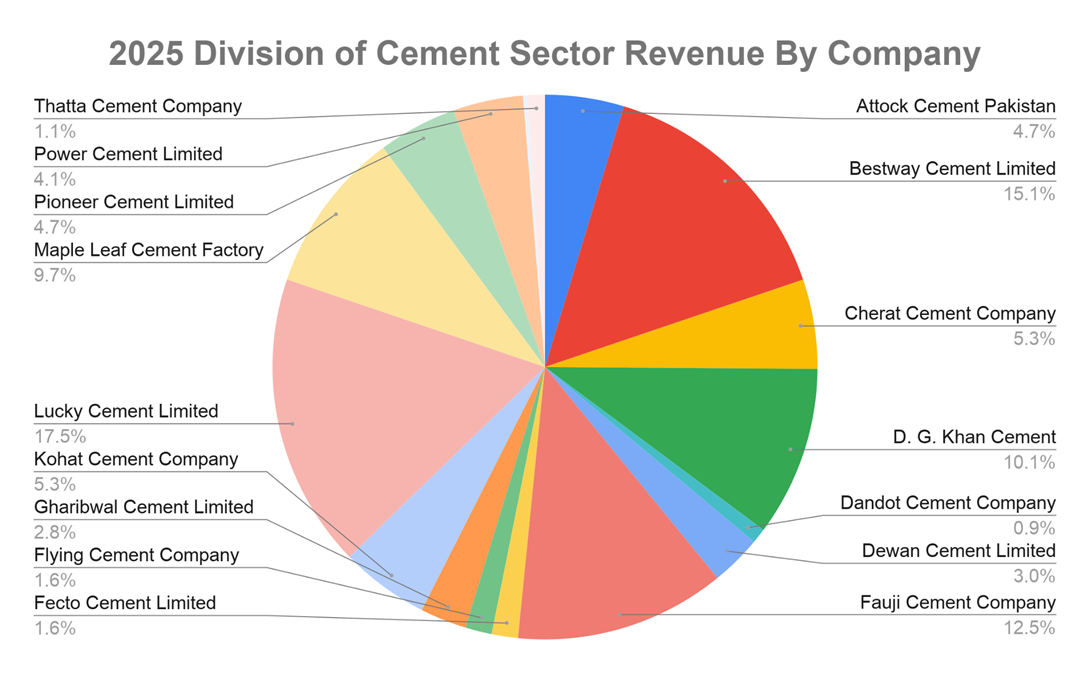

On Chart (Revenue 3), you can see the latest makeup of the current market with respect to the Revenue and on the following chart will show the breakdown of revenue by individual companies. With the biggest players being Lucky Cement (17.5%) followed by Bestway Cement (15.1%) and then Fauji Cement (12.5%).

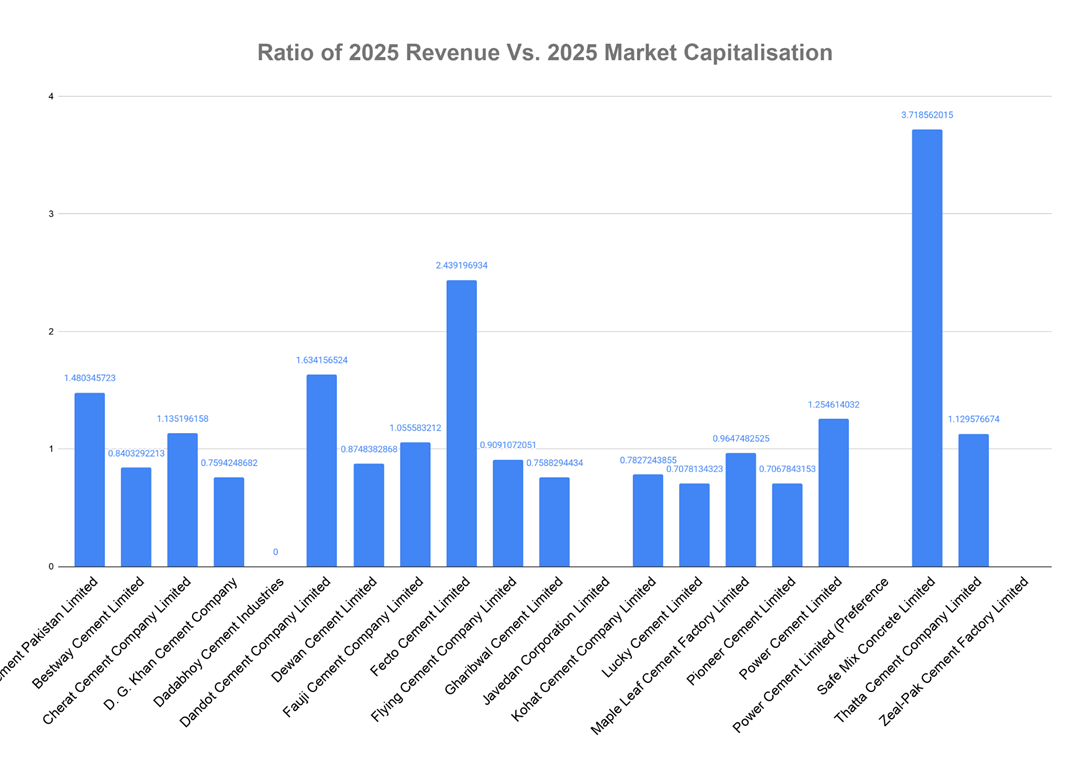

An interesting thought occurs where you compare the ratio of revenue in the sector (Revenue 4) to the market capitalization of every company in the sector (Revenue 3).

It is a surprising comparison when it comes to revenue contribution vs. market capitalization in the cement sector of Pakistan. As the top most companies in Market capitalization are contributing on a lower ratio than their less capitalized counterparts. Here smaller companies are outcompeting their larger, more established counterparts. Here Safe Mix Concrete is leading the charge followed by Fector Cement Company and then by Dandot Cement Company Limited. This becomes evident in the following table.

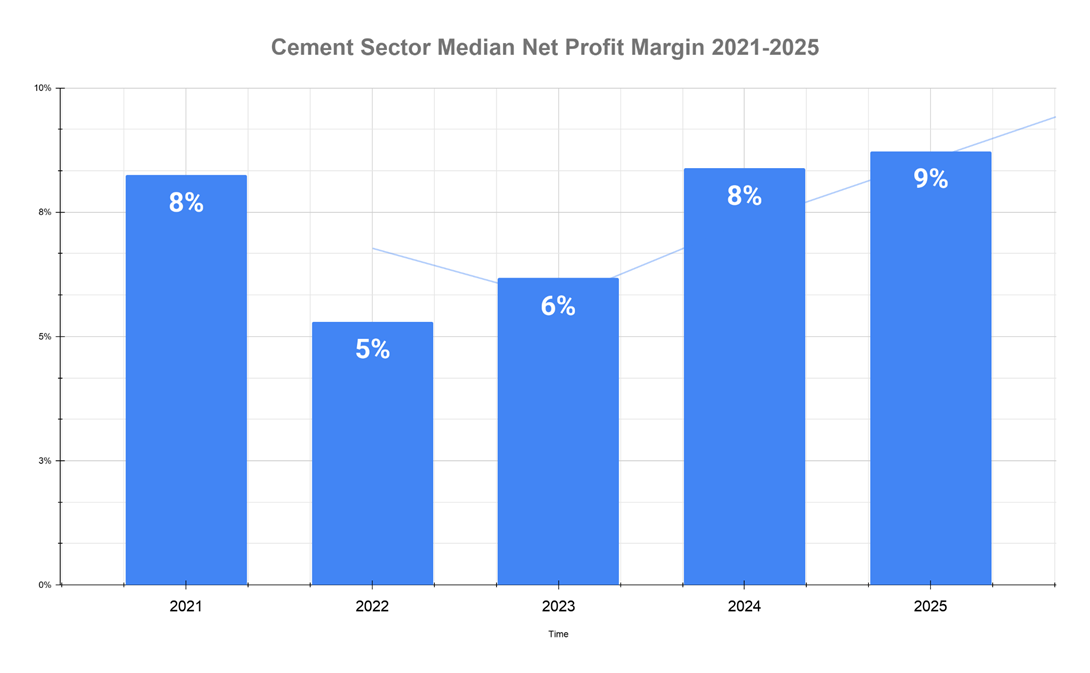

The net profit margin of these companies is varying with significant deviation. The pattern is not dependent upon size, market cap revenue generated by the company. However, provided with the average and the median of the net profit margin across time, the pattern emerges on an industry average of 8% in net profitability. However, this number is high subject to the subsidy the federal government provides. The drop in 2022-2023 was felt across the entire industry. This was due to the international increase in oil price, which is the bottleneck resource for the entire industry. Recently using modern fuel mixes, and alternative method of electricity production such as solar, the profitability has increased of the overall industry.

The cement sector in Pakistan, with its modernization and moving to alternative sources for its electricity needs has grown in the last 5 years, but the pattern that emerges shows very clearly the revenue growth has been reducing with every year that passes and the net income that only increases as the government pumps monetary support in to the industry to further its ability to grow. With the raw material, such gypsum and lime, being mined further away than in previous years, leading to further complications in the supply chain of the industry and a further increase in cost. This increase in cost, and the global market price becoming fairly competitive is the point of balance that economists and financial experts of Pakistan and the cement sector itself are trying to outplan. It is a race against all odds, especially time.

Disclaimer: This content is published solely for awareness, educational, public information, and journalistic purposes. All data is sourced from Pakistan Stock Exchange (dps.psx.com.pk) and relavant companies website.