The Food & Beverage sector remains the defensive cornerstone of the Pakistan equity market, demonstrating structural resilience during the unprecedented macroeconomic volatility of 2021–2025. Over this period, we have observed a fundamental structural pivot: the industry transitioned from a "volume-led growth" model to a "value-led survival" strategy. As domestic purchasing power was eroded by 30%+ inflation and aggressive PKR devaluation, the documented sector moved toward margin protection through premiumization, aggressive cost optimization, and a strategic "Export-First" orientation. This report analyzes the evolution of 22 key listed entities as they navigated the "Perfect Storm" of 2023 to emerge as leaner, more efficient manufacturing hubs by late 2025.

Corporate Landscape: Key Market Participants

| Company Name | Core Business Activities |

| National Foods Limited (NATF) | Spices, recipe mixes, ketchups, and desserts; leading export-led turnaround. |

| Unity Foods Limited (UNITY) | Edible oils (Dastak), fortified flour (Sunridge), and confectionery. |

| Ismail Industries Limited (ISIL) | Multi-segment leader: Confectionery (CandyLand), biscuits (Bisconni), and packaging films (Astro Films). |

| FrieslandCampina Engro (FCEPL) | Dairy powerhouse (Olper's) and tea whiteners (Tarang). |

| Fauji Foods Limited (FFL) | Dairy turnaround (Nurpur) and breakfast cereals; high-growth B2B supplier. |

| The Organic Meat Company (TOMCL) | High-value red meat processing and export-centric operations. |

| Nestle Pakistan Ltd (NESTLE) | The sector’s "Gold Standard" in dairy, beverages, and specialized nutrition. |

| Mitchell’s Fruit Farms Ltd (MFFL) | Legacy brand in preserves, squashes, and confectionery. |

| Shezan International Ltd (SHEZ) | Specialized juice and beverage manufacturer with high brand equity. |

| Matco Foods Limited (MFL) | Rice processing giant (Balky Rice) and organic sweetener exporter. |

| At-Tahur Limited (PREMA) | Premium pasteurized dairy player focused on high-margin segments. |

| Murree Brewery Company Ltd (MUREB) | Market leader in beverages and malt-based products with superior margins. |

| Rafhan Maize Products Co. Ltd (RMPL) | Industrial ingredient backbone; maize-based starches and liquid glucose. |

Strategic Utility of Comparison Metrics

To accurately assess corporate health in a high-inflation, high-interest-rate environment, we utilize six definitive metrics:

Market Capitalisation: Serves as a proxy for the "Equity Risk Premium" and the perceived defensive value of a stock as a hedge against PKR volatility.

Revenue: A measure of top-line expansion, often reflecting a company's ability to implement price hikes to offset "Cost-Push" inflation.

Net Income: The absolute indicator of bottom-line recovery following the stabilization of energy and raw material costs.

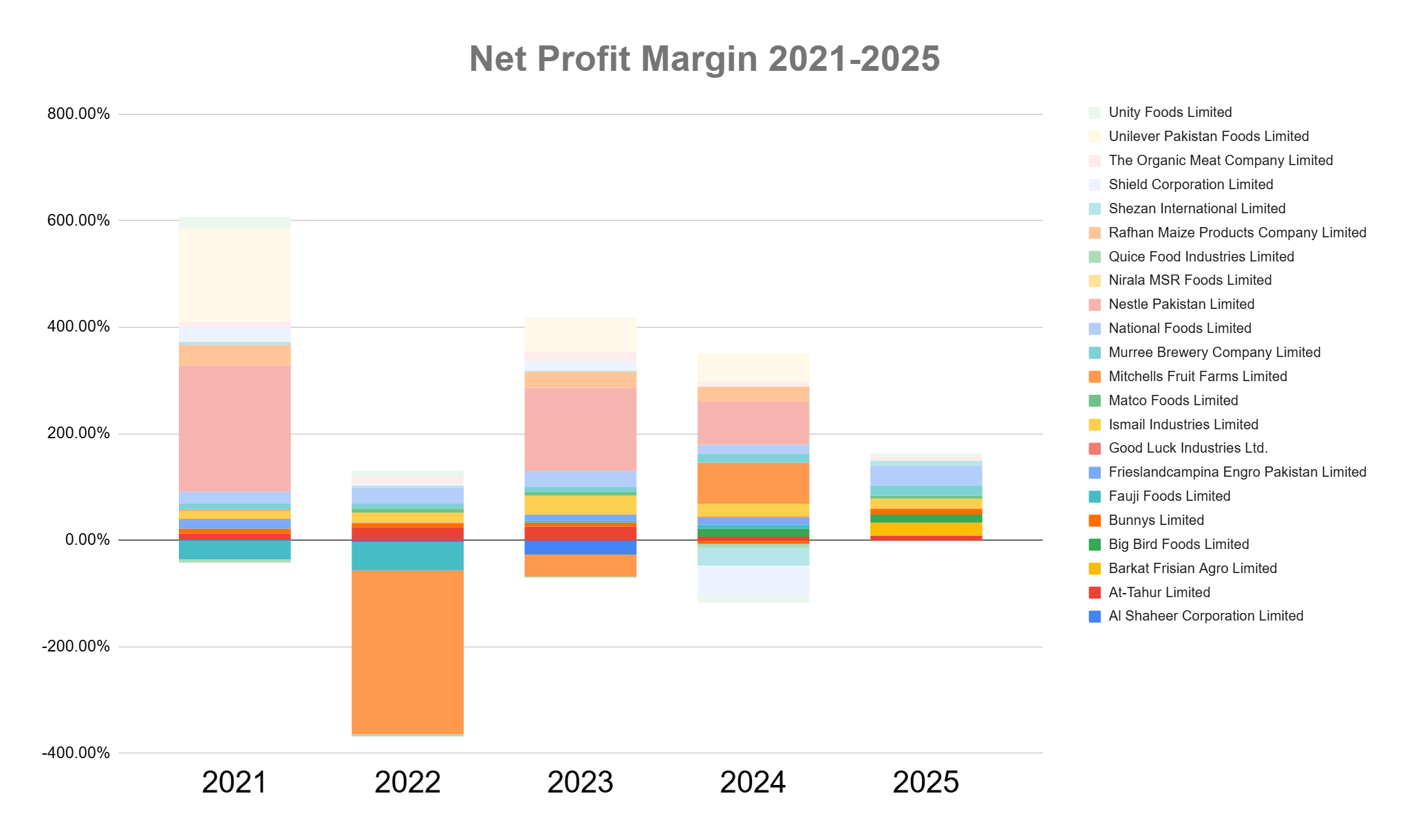

Net Income Margin: The ultimate litmus test for pricing power; it reveals if a management team can successfully pass on 30%+ inflationary costs to the end consumer.

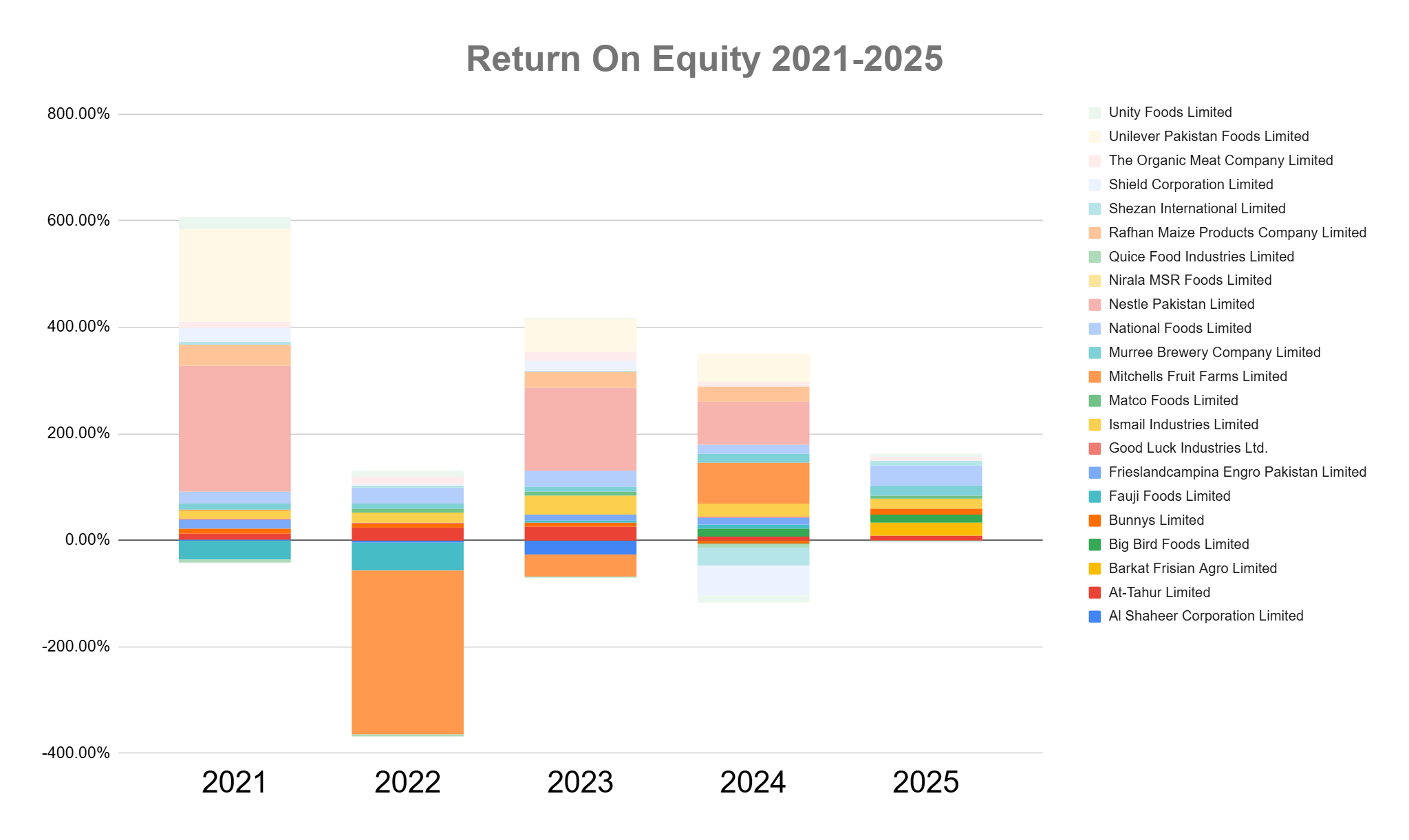

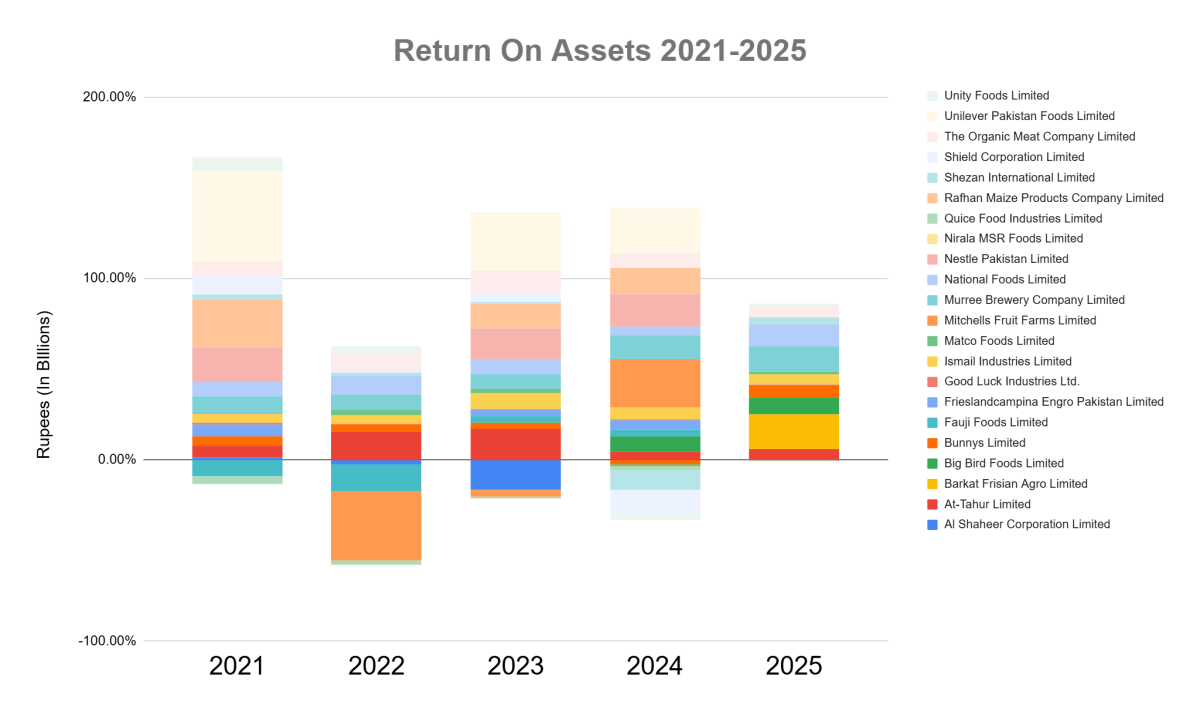

Return on Equity (ROE) & Return on Assets (ROA): These are critical markers of management efficacy in an era where the cost of debt has surged, highlighting those who can generate alpha without over-leveraging.

As structural valuations shift, it is clear that the market is increasingly rewarding entities that prioritize efficiency and export-earned "hard currency" over domestic volume.

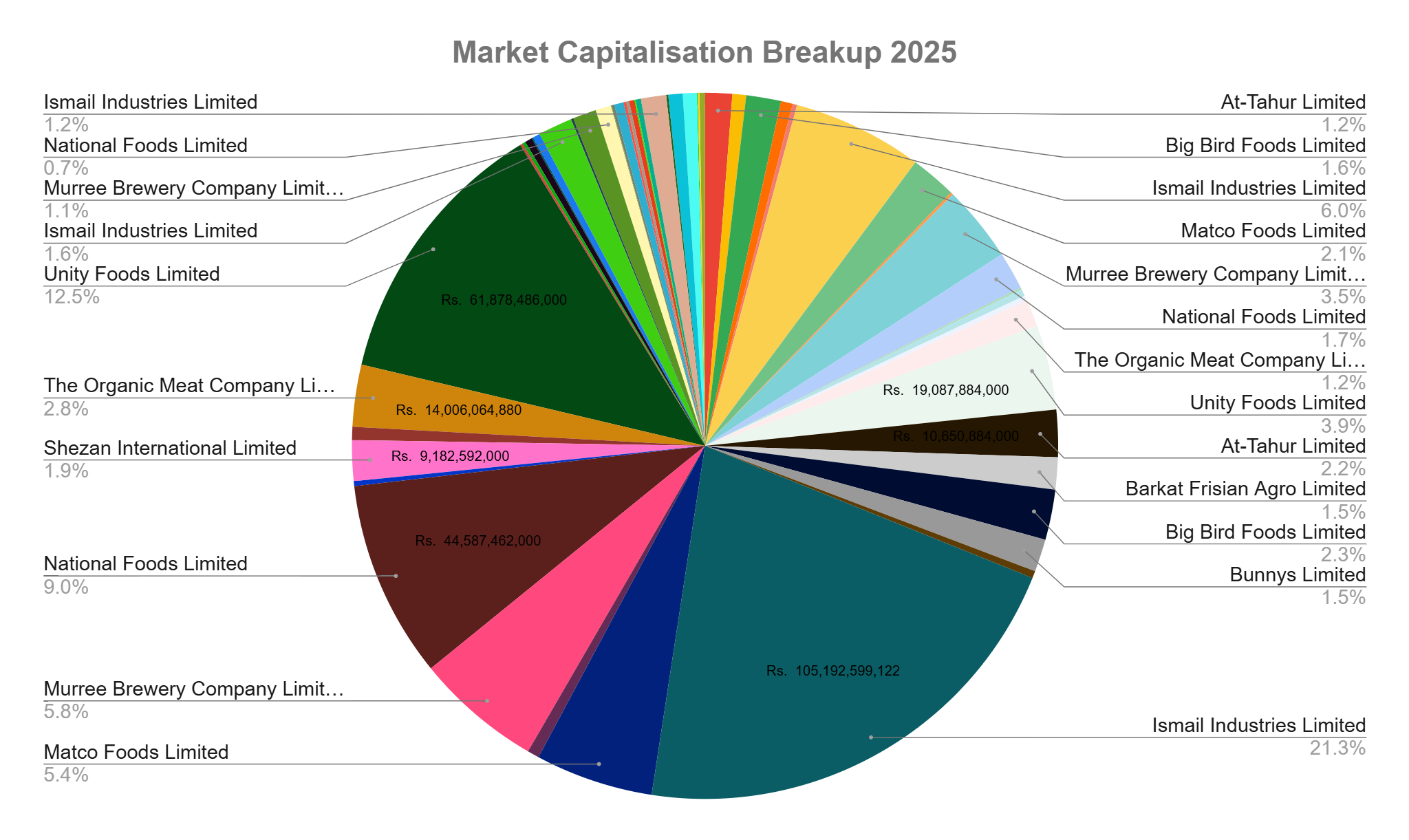

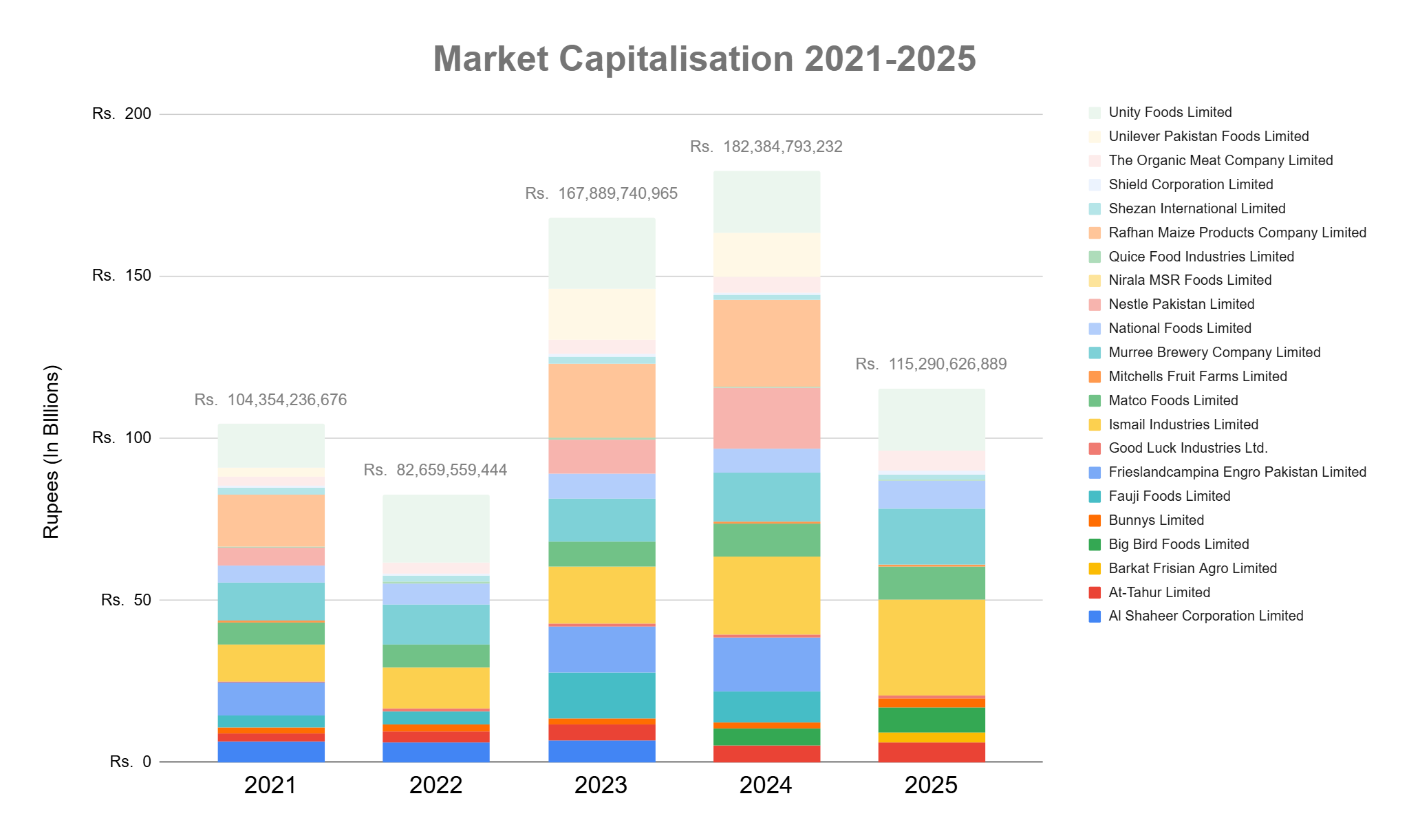

Market Capitalisation Analysis

Investor sentiment toward the edible products sector has undergone a clear bifurcation. As the PKR faced historic devaluation, capital pivoted sharply toward "Export-Heavy" and "Defensive" stocks. Investors moved away from entities reliant solely on domestic consumption toward those capable of capturing international "Dollar/Euro" revenue streams.

Sector-Wide Trends (2021-2025)

The sector opened 2021 with a "Bullish" post-pandemic stance, supported by low interest rates. However, 2023 marked a "Bearish" disruption as devastating floods and a sharp implementation of the 18% sales tax favored the informal market, squeezing documented players. By 2025, a recovery rally emerged, specifically targeting "Turnaround Stories" and companies with energy-efficient, localized supply chains.

Identification of Gains and Declines

Ismail Industries Limited: A standout performer, ISIL captured significant market share, with its valuation surging from ~Rs. 11.27B in 2021 to ~Rs. 29.42B in 2025. This growth is underpinned by the dominance of its confectionery and packaging film divisions (Astro Films), providing stable cash flows.

Murree Brewery and TOMCL: Murree Brewery maintained its profile as a high-margin cash cow, growing valuation to Rs. 17.24B. The Organic Meat Company (TOMCL) more than doubled its market cap (Rs. 2.74B to Rs. 6.16B), buoyed by aggressive expansion into Chinese and GCC markets.

Erosion of Value: Al Shaheer Corporation Limited saw its valuation drop to Rs. 0 by 2024, signaling a total exit or delisting from the documented trade. Mitchell’s Fruit Farms remains volatile, struggling to regain its 2021 peak of Rs. 836M, currently hovering around Rs. 580M.

These valuations are fundamentally anchored to the operational ability of these leaders to maintain revenue growth despite the domestic "cost-of-living" crisis.

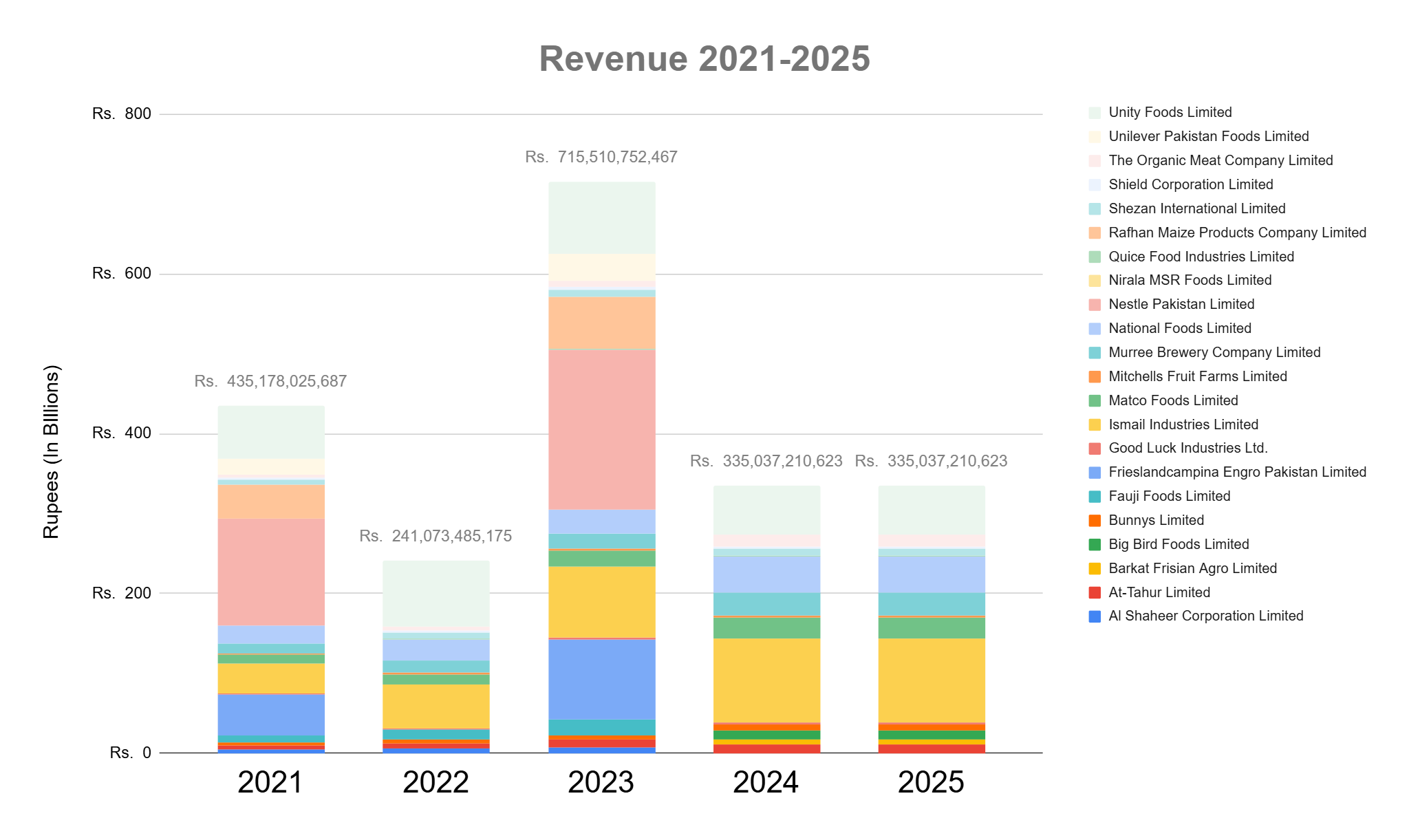

Performance Analysis: Revenue and Net Income Trends

Between 2022 and 2024, the sector faced a severe "Cost-Push" struggle. Management teams were forced to utilize aggressive pricing strategies to maintain top-line integrity as raw material and energy costs spiked.

Revenue Trend Analysis

The Revenue Giants: Nestlé Pakistan remains the sector's behemoth, crossing the Rs. 200B mark in 2023. Despite reporting lags in certain 2025 tables, interim data confirms a resilient Rs. 199.1B revenue in 2025. Ismail Industries demonstrated explosive growth, surging from Rs. 37B in 2021 to over Rs. 105B by 2025.

The "Snackification" Driver: Changing lifestyle habits catalyzed a boom in ready-to-eat segments. Fauji Foods (reaching Rs. 28.9B in 2025) and Ismail Industries captured this trend, moving away from commodity products toward high-margin branded snacks and cereals.

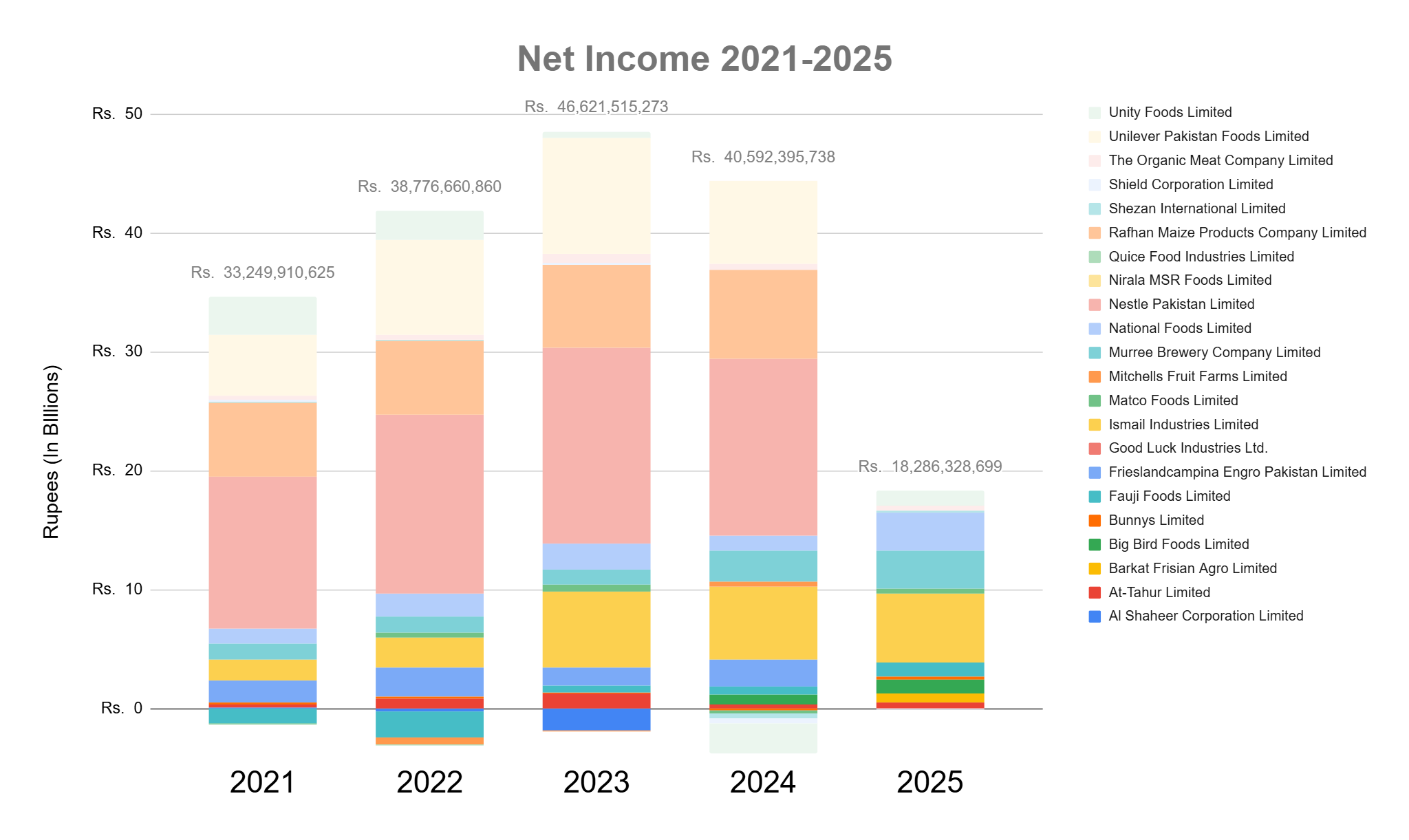

Net Income and Recovery Analysis

The Turnaround Stars: National Foods delivered a spectacular performance in 2025, recording a 795% YoY earnings jump (EPS rising from Rs. 5.44 to Rs. 13.65). This was driven by the operational efficiencies of their new Faisalabad plant and a surge in spice exports. Fauji Foods successfully executed a "Comeback Kid" story, pivoting from deep losses to a Rs. 1.15B profit in 2025, aided by the "House of Nurpur" rebranding and a robust B2B supply chain (supplying KFC/McDonald's).

Volatility and Deleveraging: Unity Foods serves as a cautionary tale of "profitless growth," swinging from a Rs. 3.1B profit in 2021 to a Rs. 2.5B loss in 2024. While 2025 shows stabilization (Rs. 1.22B profit), their high Debt-to-Equity ratio remains a monitoring point for analysts.

Performance Ratio Analysis

In the "Efficiency Era" of 2025, margin analysis has replaced pure revenue as the primary metric for equity valuation. Companies that deleveraged and localized their supply chains outperformed.

Margin Evaluation

The Gold Standard: Nestlé Pakistan maintained its premium status with consistent Gross Margins of 35-36%, a testament to its supply chain optimization. Rafhan Maize continues to act as a "dividend machine," maintaining high efficiencies with ROE/Net Margins consistently in the 27-39% range.

Efficiency Gains: Murree Brewery utilized its pricing power to increase net margins to 18.9% by 2025. Conversely, Unity Foods’ struggle in 2024 highlighted the risks of high leverage (Debt-to-Equity ~2.4x) when interest rates remain elevated.

Return on Investment (ROE/ROA)

Blue-Chip Performance: Unilever Pakistan Foods and Nestlé Pakistan remain the "safe havens" for smart money, with Nestlé hitting a staggering 155% ROE in 2023.

The Export Pivot: The strategic move toward international sales significantly bolstered the ROE for National Foods (reaching 37.38% in 2025) and The Organic Meat Company. By earning in foreign currencies, these companies successfully hedged against the PKR devaluation that eroded the returns of purely domestic players.

SWOT Analysis: Industry-Level Assessment

The industry has reached a "New Normal." Success is no longer defined by volume, but by the ability to navigate high energy costs and the competitive disadvantage against an informal market exempt from the 18% sales tax.

STRENGTHS

Resilient Defensive Nature: Inelastic demand for food ensures stable baseline consumption.

High Brand Equity: "Household names" like Nestlé, National, and Olper’s command superior pricing power.

Technological Advancement: Investments like National Foods’ Faisalabad plant have significantly reduced production waste and costs.

WEAKNESSES

High Leverage: Growth-oriented firms remain vulnerable to high interest rates (Unity Foods).

Import Vulnerability: Ongoing reliance on imported specialized ingredients creates exposure to PKR volatility.

OPPURTUNITIES

Aggressive Export Focus: Captured through major wins like TOMCL’s $7.5M order from China and National Foods’ $20M+ international sales.

Snackification & Premiumization: High-margin growth in branded cereals and organic dairy (At-Tahur).

Supply Chain Localization: Initiatives like National Foods’ "Seed-to-Table" project for tomato paste mitigate import reliance.

Energy Transition: Widespread adoption of Solar and Biogas to decouple from rising utility tariffs.

THREATS

Macro-Turbulence: Persistent PKR devaluation and potential supply chain shocks from climate events (e.g., recurrence of 2023 floods).

Tax Arbitrage: Documented players face significant margin pressure compared to the informal sector’s 18% tax advantage.

Final Summary: The Pakistan edible products sector has emerged from the 2023 crisis as a more sophisticated, export-oriented industry. With a focus on energy self-sufficiency and high-margin "snackification," the sector offers strong long-term investment appeal, specifically for players who have successfully pivoted toward the global Pakistani diaspora and international markets.

Disclaimer: This content is published solely for awareness, educational, public information, and journalistic purposes. All data is sourced from Pakistan Stock Exchange (dps.psx.com.pk) and relavant companies website.