The oil and gas exploration and production (E&P) sector remains the strategic cornerstone of Pakistan’s energy security and a heavyweight constituent of the national capital markets. Between 2021 and 2025, the sector underwent a period of significant valuation expansion; marked by a staggering 82.94% growth in aggregate market capitalization, even as it navigated the complexities of global commodity price volatility and domestic structural challenges. This report serves as a multi-year performance review of the four listed giants that define the industry’s frontier.

The sector is comprised of four major companies, differentiated by their asset bases and operational focuses:

Major Sector Constituents and Business Activities

| Company Name | Core Business Activities | Primary Operational Focus |

| Mari Energies Limited | Hydrocarbon exploration and production. | Operates the Mari Gas Field; primary supplier to the fertilizer sector. |

| Oil & Gas Development Company Limited (OGDCL) | Large-scale drilling and production. | National market leader with a diversified portfolio across all four provinces. |

| Pakistan Oilfields Limited (POL) | Exploration, drilling, and refining. | Focused on high-yield assets in the Potohar region; maintains a nimble operational footprint. |

| Pakistan Petroleum Limited (PPL) | Exploration and production. | Pioneer of the Sui gas field; extensive upstream interests in Sindh and Balochistan. |

To assess the financial health and investment viability of these entities, this report utilizes a 360-degree methodological framework centered on six metrics:

- Market Capitalisation: The aggregate market value of equity, serving as a pulse for investor sentiment.

- Revenue: Gross top-line earnings, reflecting output volume and realized price levels.

- Net Income: Bottom-line profitability after all operational costs, taxes, and royalties.

- Net Income Margin: A conceptual measure of profitability relative to revenue, indicating cost-control efficiency.

- Return on Equity (ROE): The efficiency of generating profits from shareholder capital.

- Return on Assets (ROA): A conceptual assessment of how effectively a firm utilizes its asset base to generate earnings.

By synthesizing these metrics, we establish a comprehensive view of the sector’s resilience and transition from peak earnings into a cyclical correction.

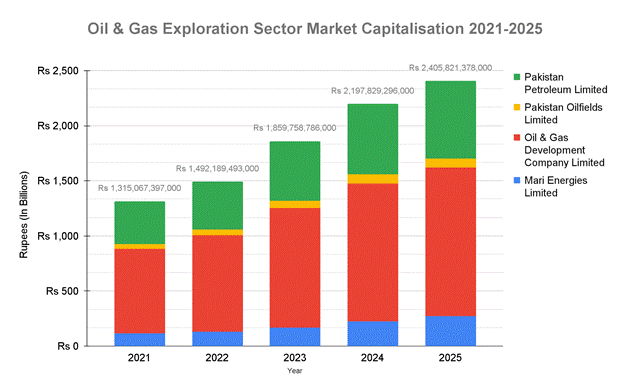

Market Capitalisation Analysis

Market capitalization serves as the ultimate barometer of institutional confidence, pricing in future cash flow expectations and the perceived risk of the domestic energy landscape. Over the five-year review period, the sector demonstrated remarkable valuation resilience, with the aggregate market cap rising from Rs. 1.3 Trillion in 2021 to Rs. 2.4 Trillion in 2025, a total expansion of 82.94%.

Oil & Gas Development Company Limited (OGDCL) maintained its status as the sector’s primary bellwether. A landmark moment occurred in 2023 when OGDCL’s valuation crossed the psychological Rs. 1 trillion threshold, eventually settling at Rs. 1.348 trillion by 2025. While OGDCL represents volume, Mari Energies Limited represented the sector’s primary growth engine, more than doubling its valuation from Rs. 115.5 billion in 2021 to Rs. 271.6 billion in 2025.

However, the final year of the study suggests a plateauing of sentiment. Pakistan Oilfields Limited (POL) saw its valuation retreat from Rs. 82.8 billion in 2024 to Rs. 80.1 billion in 2025. This divergence underscores a shift where investors are increasingly favoring the scale of OGDCL and the consistent delivery of Mari over the smaller, more volatile players.

This valuation trajectory highlights a sector that remains a high-conviction play for investors, even as fundamental growth begins to decelerate.

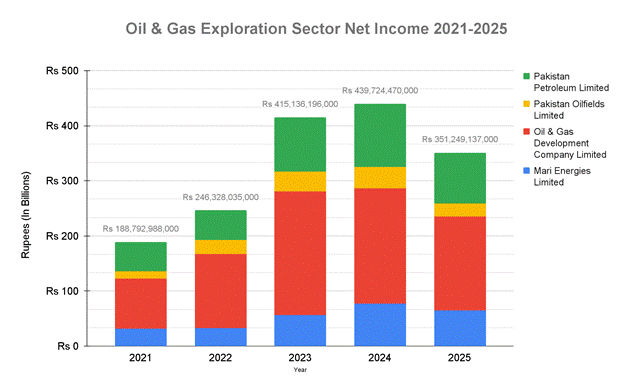

Performance Analysis: Revenue and Net Income Trends

The operational fortunes of Pakistani E&P firms are inextricably tied to global crude benchmarks and government-regulated gas pricing. The period under review saw an aggressive top-line expansion followed by a universal correction in 2025.

Sector-wide revenue surged from Rs. 496.6 billion in 2021 to a peak of Rs. 999.6 billion in 2024. However, 2025 marked a definitive turning point as revenue contracted to Rs. 877.9 billion, a dip felt by every constituent in the sector. Net income followed a similar arc, peaking in 2024 at Rs. 439.7 billion before cooling to Rs. 351.2 billion in 2025.

A nuanced look at the data reveals that Mari Energies Limited demonstrated superior earnings consistency compared to the market leader. While OGDCL saw its net income peak early in 2023 (Rs. 224.6B) and begin a decline in 2024, Mari Energies successfully grew its bottom line through 2024 (reaching Rs. 77.2B) before the 2025 correction. Pakistan Petroleum Limited (PPL) and POL also mirrored this peak-and-correction cycle, confirming that the 2025 downturn was a sector-wide macro event rather than a company-specific failure.

The 2025 performance serves as a "neutral" signal, suggesting that the era of easy, price-driven growth has concluded, necessitating a focus on operational leaness.

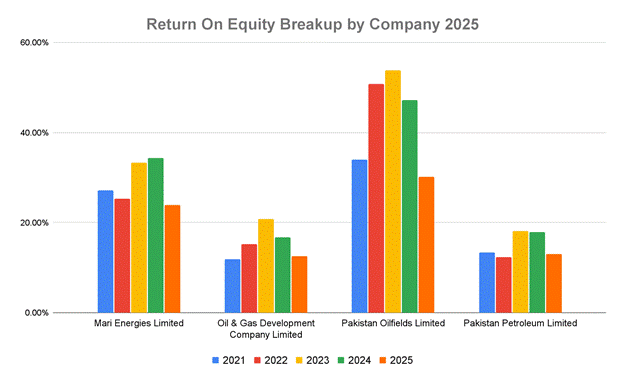

Performance Ratio Analysis

In a capital-intensive industry, efficiency ratios provide the critical lens through which we judge management's ability to extract value from assets during periods of revenue compression.

The sector’s Return on Equity (ROE) reached an institutional high of 1.26 (combined factor) in 2023. By 2025, however, this metric compressed to 0.798. This compression suggests that the sector is struggling to maintain the same level of profitability on its expanded equity base, likely due to the combined effects of falling realized prices and the ongoing circular debt issues that plague the Pakistani energy chain.

Pakistan Oilfields Limited (POL) remains the standout performer in terms of Efficiency. Despite its smaller market cap, POL achieved an ROE of 0.538 in 2023 and maintained a 0.30 ROE in 2025, significantly higher than the larger OGDCL (0.126) or PPL (0.130). POL’s ability to maintain higher returns suggests a more nimble capital structure and lower overhead compared to its state-backed peers. Conceptually, while the source does not provide direct Net Profit Margin or ROA figures, the sharp compression in ROE acts as a surrogate indicator for a sector-wide squeeze on margins and asset turnover.

The outlook for efficiency is cautious; without a significant discovery or a rebound in global prices, returns on capital are likely to remain under pressure.

Sector-Wide SWOT Analysis

This strategic assessment synthesizes our quantitative findings into a qualitative outlook for the 2025–2026 fiscal cycle.

Strength

- Dominant Market Valuation: A combined market cap exceeding Rs. 2.4 trillion provides significant stability and institutional weight.

- Historical Cash Generation: Proven ability to generate nearly Rs. 1 trillion in annual revenue, providing a deep reservoir of retained earnings.

- Strong Growth in Niche Players: Mari Energies’ 5-year trajectory demonstrates that focused asset management can outperform broader market trends.

Weakness

Efficiency Compression: A declining ROE (falling from 1.26 to 0.798) indicates diminishing returns on shareholder capital.

- Operational Sensitivity: High vulnerability to cyclical energy shifts, as evidenced by the synchronized 2025 revenue dip.

Opportunity

- Technological Reinvestment: Utilizing the massive profits of 2023–2024 to fund deep-water exploration or enhanced oil recovery (EOR) technologies.

- Consolidation and Optimization: The high efficiency of smaller players like POL suggests that larger firms have significant room for administrative and operational streamlining.

Threat

- Universal Correction: The 2025 downturn across all four firms suggests macro-economic headwinds that may persist beyond a single fiscal year.

- Asset Underutilization: If revenue continues to contract, the high fixed-cost nature of the E&P sector will lead to further ROA and margin erosion.

Pakistan Oil & Gas Exploration sector remains a high-value pillar of the financial market, characterized by its impressive 82.94% five-year valuation growth. However, the 2025 data serves as a clear cautionary note. The transition from the "super-cycle" of 2023 to the compression of 2025 indicates that the sector is moving into a defensive phase. Investors should prioritize "nimble" efficiency, as seen in POL, or the consistent profit growth shown by Mari Energies, over purely volume-driven scale in this volatile environment.

Disclaimer: This content is published solely for awareness, educational, public information, and journalistic purposes. All data is sourced from Pakistan Stock Exchange (dps.psx.com.pk) and relavant companies website.